Fooled by the seasons

Fooled by the seasons

The Fed has been wrong-footed by early-year price resets

EARLIER THIS YEAR, we noted the aggressive disinflation across major economies in the latter half of 2023 after strong first half inflation readings.

The challenge for policymakers was thus: “if price setting becomes more clustered and aggressive earlier in the year again [in 2024], then although base effects will remain favourable, allowing core to fall in YoY% terms, we could still see a sequential pick up in H1… that could just as easily roll off again into late-2024.”

And it would indeed appear that, as in 2023, this year has witnessed a certain “seasonality” in post-pandemic price setting early in the year. And this inflation strength has now rolled off as we enter the second half, putting the fed on course to hit target in the next year.

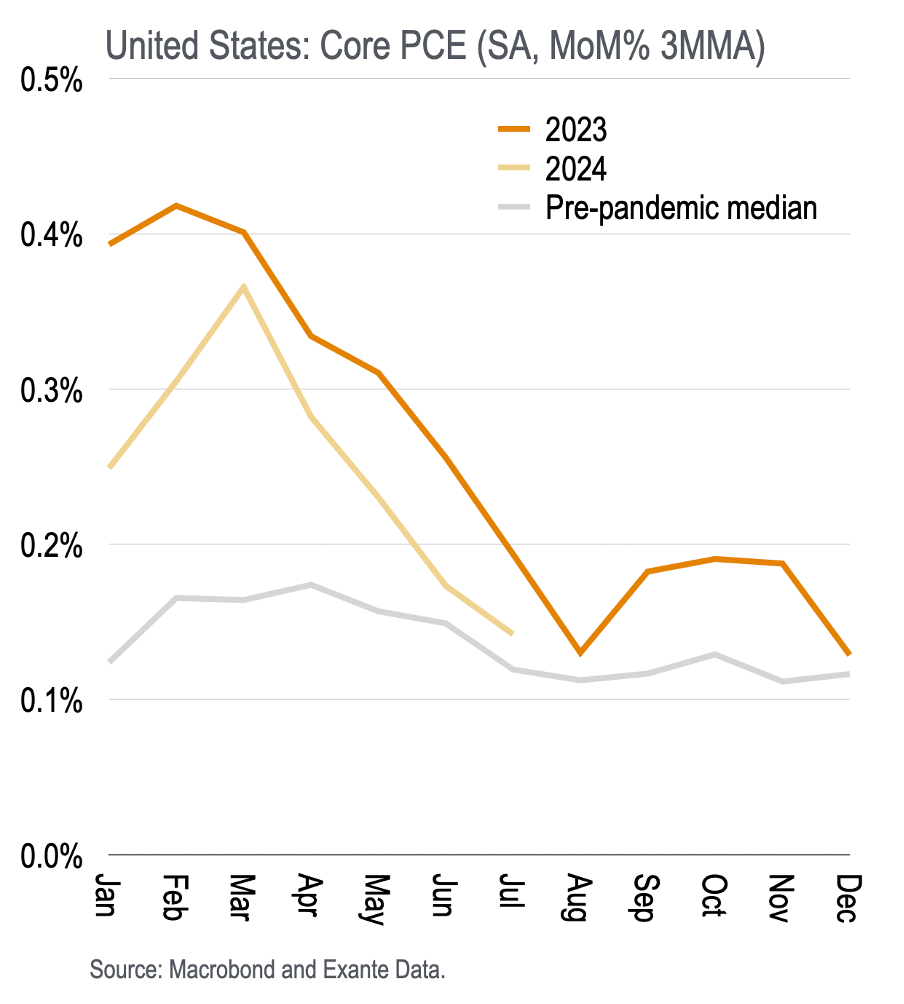

Core PCE

This seasonality is visible in the 3-month moving average of the MoM% change in (seasonally adjusted!) Core PCE.

The pre-pandemic median of MoM% inflation was reasonably flat throughout the year, though still sees some front-half bias. But in 2023, core accelerated in the first quarter (coming out of a strong 2022, of course) before rolling off into Aug. and remaining weak for the rest of the year—except for a bounce in Sept. on legal services, sporting events and the like.

Again this year, Core PCE accelerated over the 3-months to March and has softened ever since. And this year has remained the same period in 2023.

Why should this front-loading of price pressures happen?

Perhaps individual items, subject to re-sets at the beginning of the year, are playing catch-up in light of the pandemic reflation. And price re-sets are more clustered earlier in the year. But the seasonal adjustments cannot adequately capture these re-sets, being so idiosyncratic, with new products being picked up through time.

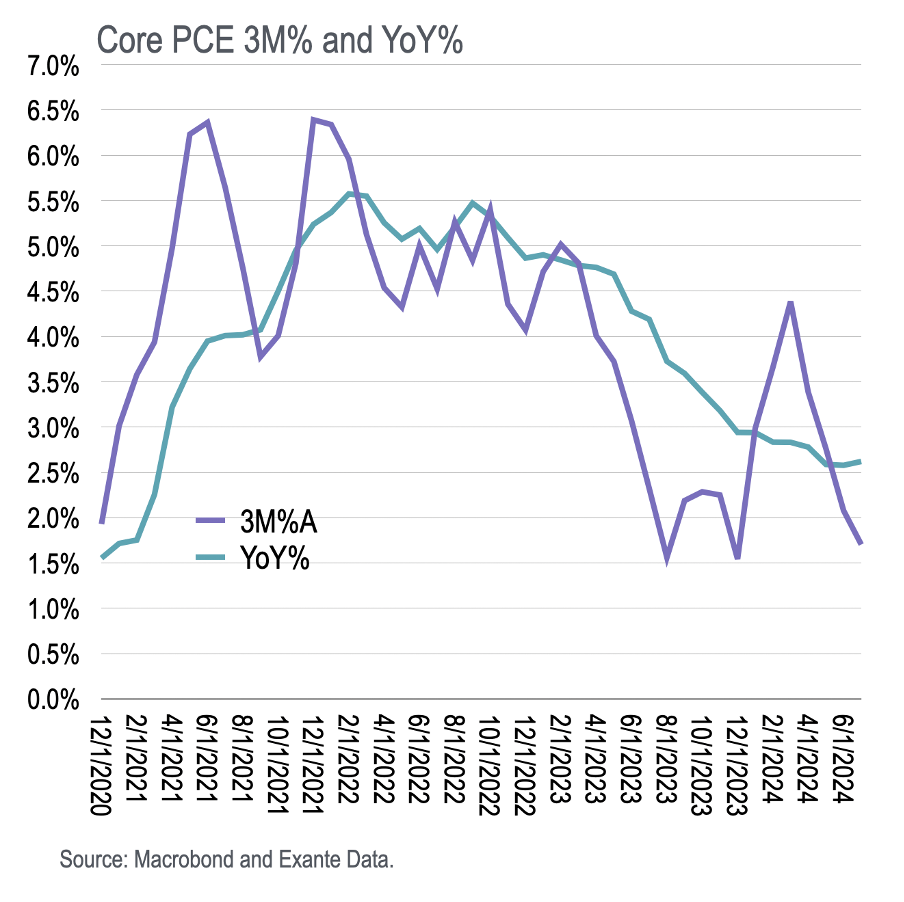

Whatever the reason, the result is also visible in the 3-month annualised Core PCE, which increased from below 2% at the end of 2023 to above 4% in March before falling back to below 2% again over the 3-months to July.

Such clustering is also visible at other phases of the pandemic reflation. But that early in the year, this year and last, might be the last throes of a remarkable and unexpected price level adjustment that is slowly working its way through the constellation of prices.

Revised forecasts

Unfortunately, the Fed reacted to the acceleration in Core PCE in the first half of this year by dialling back expectations of policy normalisation. The Dec. 2023 SEP median forecast for Core PCE, for example, was 2.4%YoY in 2024Q4 but was revised up to 2.6%YoY in March and further to 2.8%YoY in June this year.

Curiously, armed with the latest Core PCE print, it is unlikely that we will end the year with Core PCE above 2.6%YoY while the original 2.4%YoY projection could easily turn out to be spot on.

If the FOMC had not been wrong-footed by the “seasonality” of Core PCE earlier this year, they may not have revised up their forecasts—and might instead have focussed on growing risks to employment.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.