A downside surprise

A downside surprise

Eurozone Sept. Core HICP printed below expectations, a rare occurrence of late

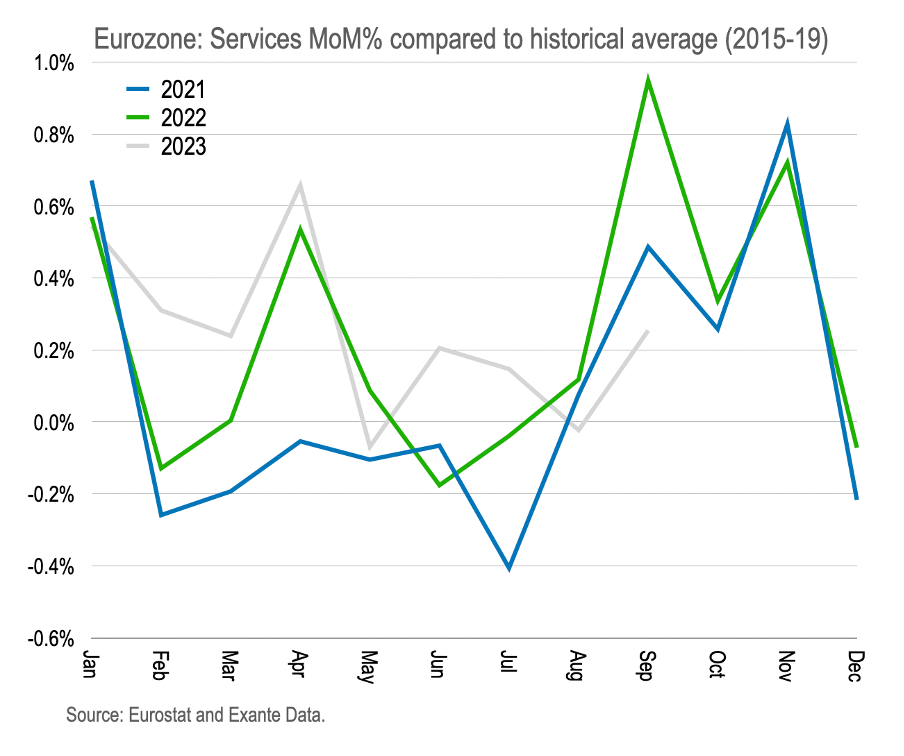

Preliminary core HICP for the Eurozone in Sep. fell to 4.5%YoY, below analyst expectations of 4.8%YoY from 5.3%YoY in Aug. Some slowdown was expected due to “base effects,” but the strength of the undershoot has been a surprise. Is there something to learn from the pattern of service sector seasonality in recent years? How will this impact service inflation later this year? And what does this say about ECB policy?

Base effects

If we look at the pattern of MoM% service inflation in the Eurozone compared to the 2015-19 average, we see striking deviations in 2021 and 2022 with stronger-than-average inflation over the period Sep. to Nov. with somewhat weaker prints earlier in the year. This is a sign of changing seasonality in service inflation, at least during the immediate post-pandemic recovery.