Argentina: Four notes on a revised program (No.1)

Argentina: Four notes on a revised program (No.1)

Note 1: Exchange rate assumptions

The IMF’s latest Staff Report for Argentina—the 7th Review under the Extended Arrangement under the EFF, on the occasion of the renegotiation by incoming President Milei—offers an opportunity to re-set a program that careered off the rails under each of the previous two governments.

Getting it right this time is more important than ever.

If Milei fails, the danger of a rotation back to the “left” once more could bring default on the outstanding IMF debt, around USD45 billion, and further drift and impoverishment for the people of Argentina.

In other words, it is crucial the international community ensures past failings are overcome.

The Staff Report is difficult summarise in a single post. So the approach here is to provide an overview of various different aspects in bite-size form.

We therefore review the document in four parts: first, exchange rate assumptions; second, central bank sustainability; third, fiscal sustainability; and fourth, external sustainability.

Photo Credit: Vick Bufano.

Exchange rate assumptions

It’s always useful to ask, when looking through IMF documents: what exchange rate path underpins the program?

This is particularly important when liability dollarisation of public debt makes exchange rate stabilization crucial for sustainability of the public sector.

Exchange rate path

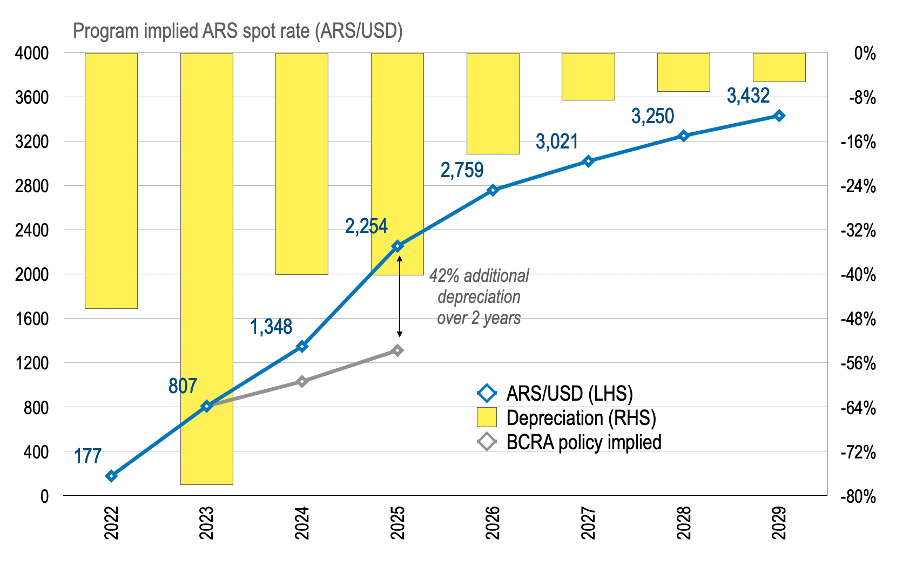

Table 7 (p. 53) of the Staff Report summaries the debt stock and dollar GDP assumptions that underpin the debt-to-GDP projection.

To back out the exchange rate underlying this projection, we need the path for nominal GDP in local currency. We use the 2022 nominal GDP in local currency from the last WEO and apply the growth of nominal GDP (see Table 5, p. 72) to get this from 2023 to 2029.

The implied exchange rate is shown in the chart below.

The exchange rate at which debt-to-GDP is calculated in 2023 is the end-year exchange rate of 807.4 ARS per USD, increasing to 1,348 by end-2024 and 2,254 by end-2025 and so on.

After depreciation of nearly 80% in 2023 (end-year), ARS is expected to depreciate roughly 40% in both 2024 and 2025 before roughly halving to 20% in 2026.

This is odd.

BCRA announced crawl

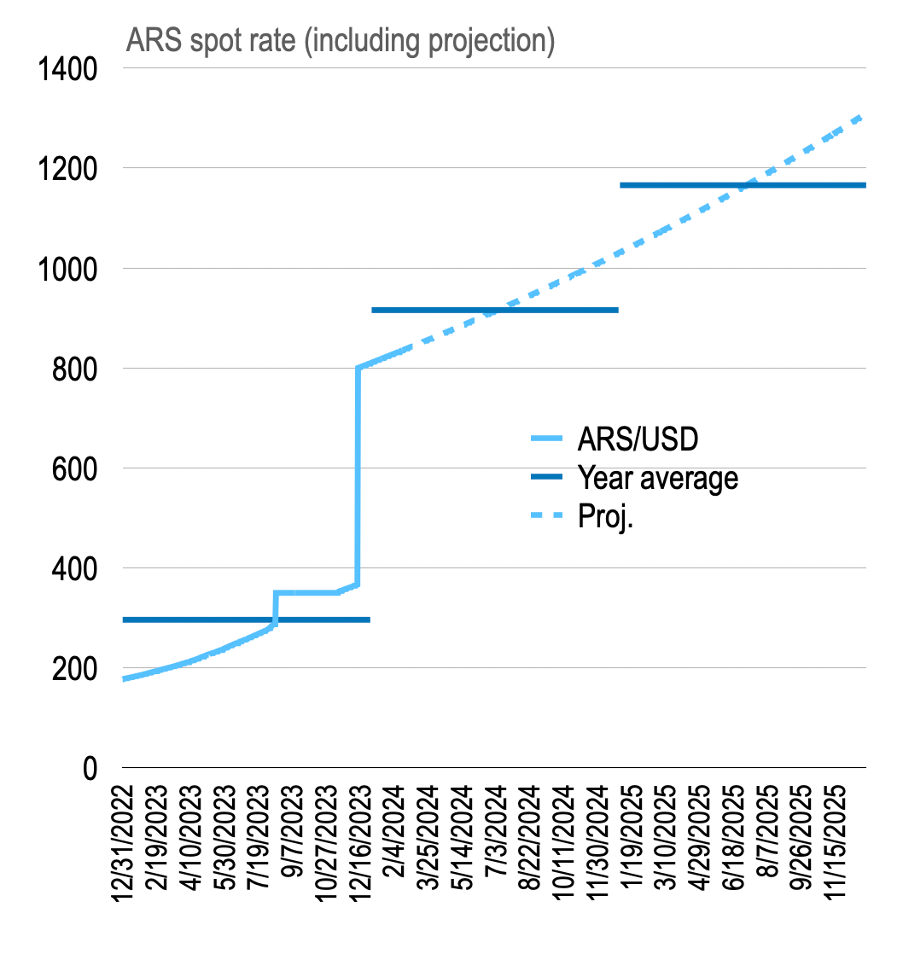

BCRA announced a 2% monthly crawl alongside the large adjustment on 13th Dec 2023 (see here.) Precisely, they explain how, “based on the current situation, the exchange rate change path is currently set at 2% monthly.” And this is the path they have been on since.

If we project forward the daily exchange rate based on recent weekly patterns, we get a continuation of the 2% monthly exchange rate depreciation (see also the final chart below) and an end-2024 nominal exchange rate of roughly ARS1,030 per USD (the year average exchange rate being ARS 915) and end-2025 of ARS1,310 (year average of ARS1,164.)

This is substantially below and so stronger than the IMF’s projected exchange rate used to construct the DSA, as shown above.

In fact, the IMF projects the exchange rate by the end of this year to be weaker than that implied by BCRA policy by end-2025 (IMF = ARS1,348 this year versus ARS1,310 according to current exchange rate policy.)

Alternatively, the Fund builds an additional 40% depreciation over the next 2 years than implied by the crawling peg announced by BCRA.

In short, the implicit exchange rate path in the program document is inconsistent with the authorities’ announced exchange rate policy.

Does this mean the Fund is projecting current policies will not hold?

What does the text of the Staff Report reveal?

This unpicks the tables that prop up the Staff Report.

It’s worth instead reviewing the document for discussion of the exchange rate, starting with the description of the devaluation episode (¶35, p.20, emphasis added):

Before the large December step devaluation of roughly 120 percent, the REER was estimated to be around 35–40 percent stronger than the level implied by medium-term fundamentals. The devaluation (moving the nominal official exchange rate from 360 ARS/USD to 800 ARS/USD) enabled an initial real overshooting, which has been instrumental in immediately rebuilding reserves and averting a balance of payments crisis. Following the exchange rate overshooting, the authorities set the initial official crawl rate at 2 percent per month to help anchor inflation, while communicating that fiscal policy remained their primary policy anchor.

We immediately encounter a confusion.

The currency did not devalue 120% in December. Rather, the currency, correctly calculated—i.e., the change in the reciprocal of the number of ARS that can be purchased per dollar—depreciated by 54%. The Fund is not calculating the devaluation correctly.

The lower figure of 54% devaluation better frames the real exchange rate adjustment discussed here; if ARS was initially overvalued by 35-40%, then the exchange rate adjusted for this with an overshooting of about 15% that might be later eroded by inflation.

In addition, regarding future exchange rate policy, we get the following remarks as part of the Staff Appraisal (¶59, pp.31-32):

Following the much-needed correction of the FX misalignment, FX policy will need to be carefully calibrated to support reserve accumulation. Care will need to be taken to avoid a rapid unwinding of the earlier competitiveness gains to secure a current account surplus consistent with reserve accumulation goals. Staff welcomes the commitment to move to a more market-based regime and the abandonment of the previous approach of intervening in the parallel and non- deliverable futures FX markets, which only drain reserves and add to vulnerabilities.

This implies more exchange rate flexibility will be needed in future if inflation remains high. Perhaps the initial depreciation-plus-crawl was not enough after all? The black market rate has this flavour.

Whatever the explanation, reading the Staff Report suggests three reasons the Fund might be projecting a path for the exchange rate inconsistent with BCRA announced policy.

The first is because staff don’t understand how to calculate the rate of depreciation of a currency.

The second is because staff do not believe recent devaluation was sufficient.

The third is because staff think the devaluation was initially sufficient, but don’t believe current crawling peg is credible and wish to deviate from this.

What does this mean?

This is pretty wild stuff.

In a highly liability-dollarized economy such as Argentina, continued exchange rate depreciation creates an additional hurdle for sustainability. The local currency value of dollar debt is continually revised up.

Alternatively, to show debt on a declining path, this requires higer-for-longer inflation—and the deprivations that go with it. And this is what is embedded in the staff report—nominal GDP growth, a good proxy for inflation, is expected to be 67% in 2025 and 37% in 2026 even after the recent devaluation will have washed out.

In other words, the program assumes no rapid stabilization of inflation.

This is a long way from Argentina’s convertibility plan in the 1990s which surprised many for the rapidity of the disinflation that followed.

Apparently Milei’s stabilisation plan will not such a success. No more Mr. Dollarisation!

What depreciation path is consistent with the program?

If the IMF really disbelieve the BCRA crawling peg, then locals should also begin to expect a more rapid depreciation.

We can conclude for now by illustrating a depreciation path consistent with the IMF program document—precisely, by assuming the current crawl continues through end-June before moving to a more rapid depreciation pace, and adjusting again in 2025.

To be consistent with the program, ARS depreciation has to shift to nearly 6% per month in the second half of this year and then about 4% all of next year.

If the exchange rate assumptions are baffling enough, the next post looks at the sustainability of BCRA balance sheet—a source of endless confusion in the past.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.