Germany's record trade surplus

Germany's record trade surplus

Move over China, Germany is back!

There has important emphasis of late on China’s record surpluses which are proving to define the post-pandemic global landscape.

Less noticed is the fact that Germany’s trade balance has over the past 6 months increased sharply—to reach a record in nominal terms.

In other words, it is not just China’s surplus that is back.

A record surplus

Last week, Germany’s monthly January trade balance, calendar and seasonally adjusted, increased by EUR4.2bn to reach EUR27.5bn which is a record monthly nominal surplus.

This external surplus has increased EUR9.2bn over the past 6 months as exports have increased EUR4.0bn while imports have contracted EUR5.3bn.

And since Dec. 2019, the trade balance surplus has therefore increased EUR7.1bn with exports up EUR23.6bn and imports up only EUR16.5bn.

This is monthly. The annualized January surplus is closer to EUR330bn.

This certainly challenges the idea that the German economy is struggling and her trade balance surplus is likely to be eroded due to competitiveness concerns.

It’s worth digging a little further into what is going on.

Destination

Starting with the regional destination for goods exports, the euroarea has seen the largest increase since end-2019 along with the US and CEE-3 as a block.

This perhaps confirms that non-Germany Europe is experiencing a recovery.

Exports to Russia are down, of course, as are Asian exports due to China.

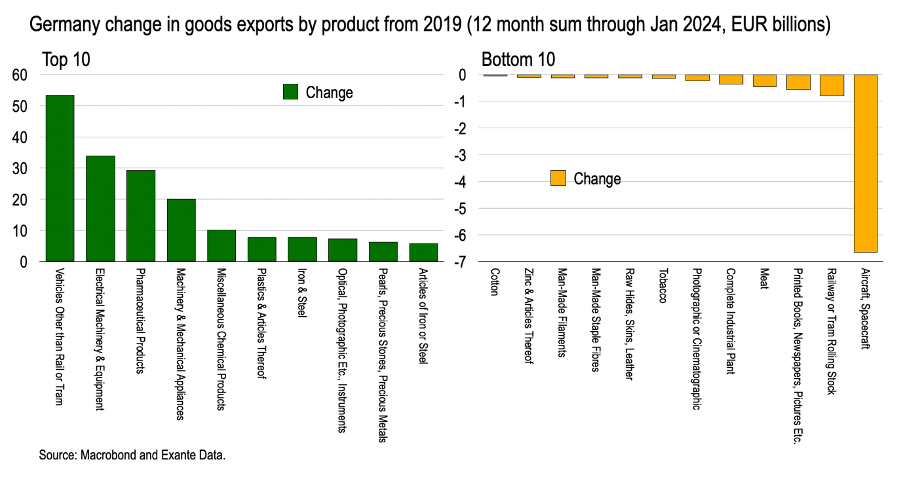

Products

Alternatively, in terms of products, the traditional categories are leading the increase: vehicles, electrical machinery, machinery and pharmaceuticals.

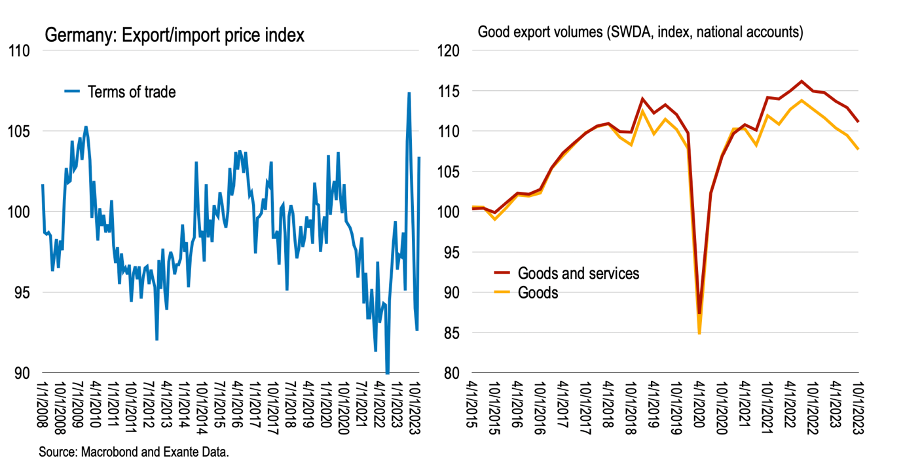

Terms of trade and real exports

Germany’s terms of trade is noisy, but lower energy prices recently has seen the relative price of Germany exports jump (through December) close to historical peaks.

Meanwhile, national accounts data shows export volumes on a secular decline.

That is, measured in real terms, German exports continue to contract. But the terms of trade has shifted to favour Germany, meaning the nominal trade balance surplus has reached a new high now that energy prices have normalized.

A short lived boost?

Our best guess here is that traditional German industries, while enjoying weak export volumes, have experienced a boost in nominal terms due to the post-pandemic surge in traded goods prices.

As noted, now that energy prices have normalised this full effect is starting to show.

We ought to scale this monthly surplus by GDP to put it in context—which the next chart does from 1971.

While there have been months when Germany’s trade balance surplus, relative to GDP, has been larger. these are only few.

And the trade balance in January is back to 8% of GDP and could increase further from here!

Moreover, a growing portion of this is bilateral with the rest of the Eurozone, as well as CEE-3 and the US.

In a sense, we are returning to the pre-GFC decade when a large part of Germany’s current account surplus was intra-Eurozone.

As such, the Eurozone current account surplus could therefore still narrow but Germany show continued strength in coming months.

Why will Germany’s surplus narrow?

For two reasons.

In terms of prices, German manufacturers could pass on lower costs due to energy prices, to claw back recent competitiveness losses. This implies traded goods could experience some deflation to offset the recent inflation.

Alternatively, in terms of volumes, German manufacturing might continue to lose out to more competitive producers, contracting secularly in real terms, eroding the future surplus. In which case, the recent terms of trade boost will prove only a temporary reprieve.

Whatever the case, it seems that Germany’s trade balance surplus, and likely current account, will be sticky for some time longer.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.