Historical Freeze of Russia's Central Bank Reserves

Historical Freeze of Russia's Central Bank Reserves

In an exceptional move, the EU and G7 CBs globally has frozen CBR's assets; where are these held and what does it mean?

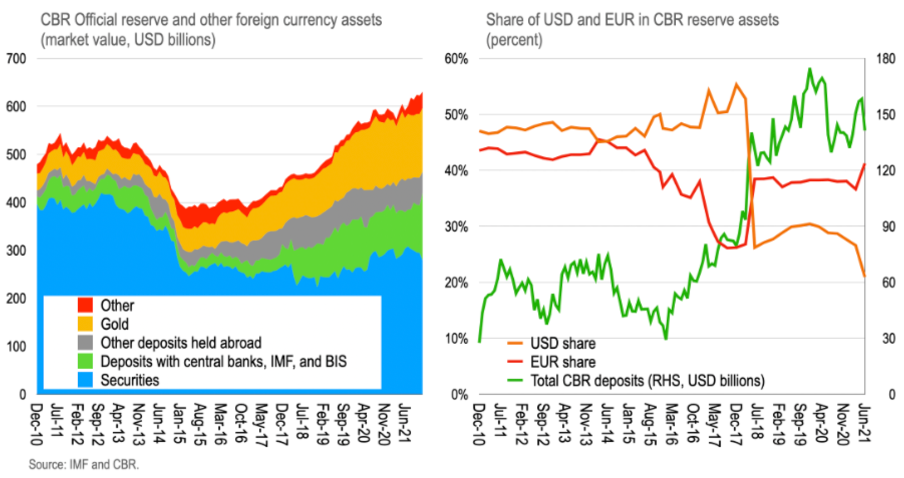

CBR international reserves are about USD630bn, of which about USD130bn are in gold held domestically and about USD500bn as various financial assets: USD300bn in securities; USD160bn in deposits; USD25bn in SDRs; and a small residual amount.

The increase in deposits held at central banks as reserves underlines how reserves have diversified out of securities in recent years due to the shortage of safe assets;

This weekend, access to about half these reserves was blocked by the European Union and United States—with Switzerland and Japan confirming they will follow suit on Monday.

This act of ‘financial diplomacy’ is designed to inflict maximum damage on the Russian economy—to facilitate an end to hostilities or regime change.

Central banks have a poor track record when it comes to appeasing European tyrants. In March 1939, after the Nazi invasion of the Czechoslovakia, Germany's Reichsbank expropriated Czech National Bank gold that had been transferred to the Bank of International Settlements (BIS) for safekeeping. This gold was then shipped abroad and sold, including to London with the support of the Bank of England—a shameful episode in the history of central banking.

Perhaps with this in mind, the decision by the European Union over the weekend, and the United States today, to immediately block the Central Bank of Russia’s (CBR’s) reserve assets represents an exceptional move designed to inflict maximum pain on the Russian economy in order to bring the conflict to an early end (and this has been part of the reason for the dramatic depreciation of the Russian Ruble, which is in motion now).

How large? And where?

CBR reserves are about USD630bn (see left chart below), of which about 1/5th (USD130bn) are in gold that is held domestically. That leaves USD500bn as financial assets, roughly: USD300bn in securities; USD160bn in deposits; USD25bn in SDRs; and a small residual amount.

Of these deposits, a decent chunk are held at central banks, the BIS, or the IMF (about USD100bn). Indeed, the deposit share of reserves increased sharply in 2018 when they were forced to sell US Treasuries (right chart). And this increase in deposits was coincident with the reported increase in the share of euros on CBR balance sheet, which is at least suggestive that these Treasuries were moved into deposits at European banks or at the Eurosystem.

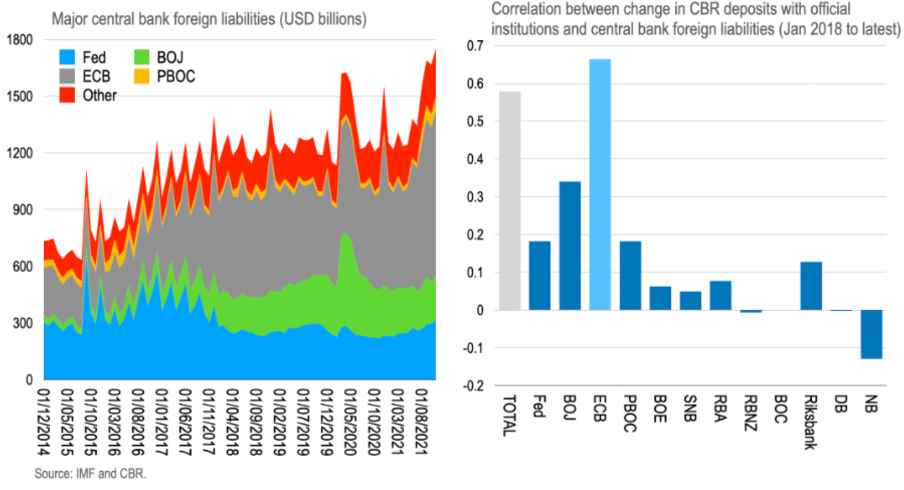

So once more, central banks play a key role in handling the foreign exchange reserves of a belligerents central bank. Can we track down which central bank they are with? The chart below shows the non-resident liabilities of the major central banks since 2014. Such deposits have increased sharply in the next decade as a shortage of safe assets forced reserve managers to seek out deposit facilities at major central banks.

One hint as to the destination of Russian deposits is in the correlation coefficient between the monthly change in these deposit liabilities and the CBR official deposit assets with central banks and the BIS. And the correlation coefficient is greatest for the Eurosystem (0.65) and much smaller for other central banks.

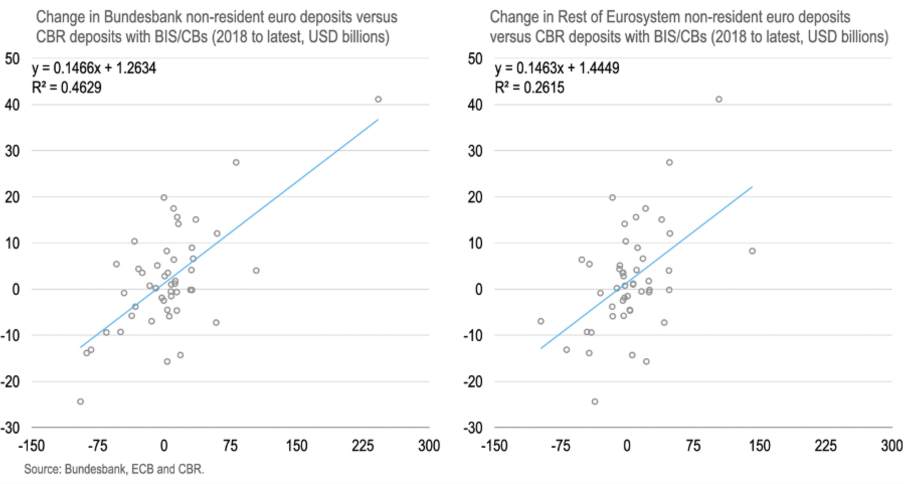

What more do we know? The next chart (below left) shows non-resident euro deposits with Bundesbank as well as the rest of the Eurosystem alongside these CBR official deposits. While the chart also shows (right) shows the 5Y rolling correlation coefficient between these, and from 2017 the correlation between the monthly change in these jumped sharply.

This is again suggestive that CBR holds deposits with the Eurosystem, and the Bundesbank in particular. There has been a growing relationship between the Eurosystem and central bank reserve managers in recent years.

Alternatively, we can look at the scatter of the monthly change in CBR official deposits and non-resident euro deposits with the Bundesbank (left) and rest of Eurosystem (right). Note the larger R^2 in the latter.

There are caveats, but we will focus on the big picture today.

But the deposits might only be fleetingly on the eurosystem balance sheet driving this correlation. In any case, second, as Zoltan Poszar of Credit Suisse argued last week, the CBR might actually have a larger dollar exposure but they don't report it. In this view, these deposits represent the euro collateral from dollar swaps by CBR. For example, RBA has large holdings of JPY but swaps it back to dollars, only they are transparent about this.

If Pozsar is right, then CBR is now doing the same, possibly in euro and yen or others, but is not revealing this in their decomposition.

Alternatively, third, CBR might simply hold euro deposits outright as an alternative to euro securities when the interest rate is too low. Indeed, there is a negative correlation between their private and official deposits, which also suggests quarter-end window dressing of a different kind, as banks push these deposits to the Eurosystem and than back to private banks outside of quarter-end.

What about the BIS?

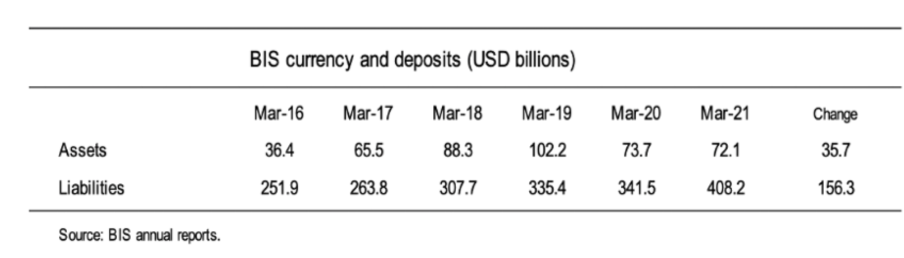

Another alternative is that these deposits moves into euros, but could be held at the BIS. Looking at the end-Q1 balance sheet snapshot from their annual reports (converted to USD) their deposit liabilities have increased about USD150bn over the past 5 years.

So in principle the BIS could be harbouring these. The BIS today said it would not be a vehicle for the sanctions to be circumvented.

Overall, no smoking gun on which central bank holds these CBR deposits. There could also be some at the Bank of Japan. But since all G7 central banks are acting now, it matters less.

But it is highly likely the CBR uses reserve manager services at the Eurosystem on occasion (year-end in particular) if not more generally. Indeed, the Bundesbank confirmed to us over the weekend if any such deposits exist, they are now frozen following the announcement over the weekend.

Together with the securities held in the Eurozone, EU foreign ministers yesterday claimed 50% of Russia’s reserves would be frozen—an unprecedented act of financial warfare in response to the aggression against Ukraine that resulted in the sharp sell off in Ruble this morning.

What happens next?

While not exactly unprecedented—Iran’s central bank was itself subject to sanctions in recent years—the actions against the CBR are exceptional as a response to an act of war. And the speed and severity of official actions in this case has never been seen before—setting a precedent for future acts of irredentism.

Perhaps the failures from the 1930s have been internalised.

This development is likely to have long run effects for global trade and payments, however.

First, for Russia, the bilateral trade and financial relations with China are likely to grow in importance. As it is one of the only routes left. The CBR renminbi assets remain accessible, as well as their gold, so there is some small buffer still (although liquidity is an issue). And in the future these two assets are likely to dominate their reserve management alongside trade.

Second, for other countries—and China in particular—the example in this case is that reserve assets might not be as safe as assumed. And if they plan to engage in military adventurism, then it would be safe to diversify out of dollars, euros, and yen and into gold and other alternatives.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.

i wonder about all the talk in favor of moving into gold. wouldn't it be almost impossible to actually sell that gold and use it to buy imports or support the domestic financial system? how do you exchange the gold for dollars when your banks dont have correspondent accounts working? or whoever deals with you is subject to secondary sanctions? reserve managers will be asking themselves how they should be using reserves to be able to actually support the domestic economy in a time of need. maybe the result will be more stockpiling of resources rather than currency reserves.