How to Manage the Dollar (Part I)

How to Manage the Dollar (Part I)

A little bit of dollar history

… the strong-dollar policy is an expression of what seems to me to be a very fundamental principle of national economic management, and that is that the strategy of artificially devaluing a currency to seek competitive or commercial advantage is, for a major industrial economy, an unsound policy that carries with it risks that are not commensurate with its benefits, and it seems to me that the strong-dollar policy understood in that way should be a constant in the policy of the United States.

Larry Summers, Per Jacobsson Foundation Lecture, October 2004

It is now nearly 20 years since Larry Summers defended the “strong-dollar policy” in his famous Per Jacobsson Lecture by suggesting, as if it is obvious, that anything otherwise would be “an unsound policy that carries with it risks that are not commensurate with its benefits.”

It is a reflection of our times that the sacrosanct strong-dollar policy, as with many other aspects of the post-war settlement, is now being reconsidered.

Indeed, as the United States Presidential election draws closer—and the prospect of a Trump 2.0 administration grows—the focus is turning to the dollar. What will be the future dollar policy?

In this post, the first of a series on the US dollar policy ahead, we begin by highlighting some dollar history.

From Bretton Woods to Louvre

Since President Nixon suspended dollar convertibility to gold in 1971, we have seen US dollar policy gradually evolve.

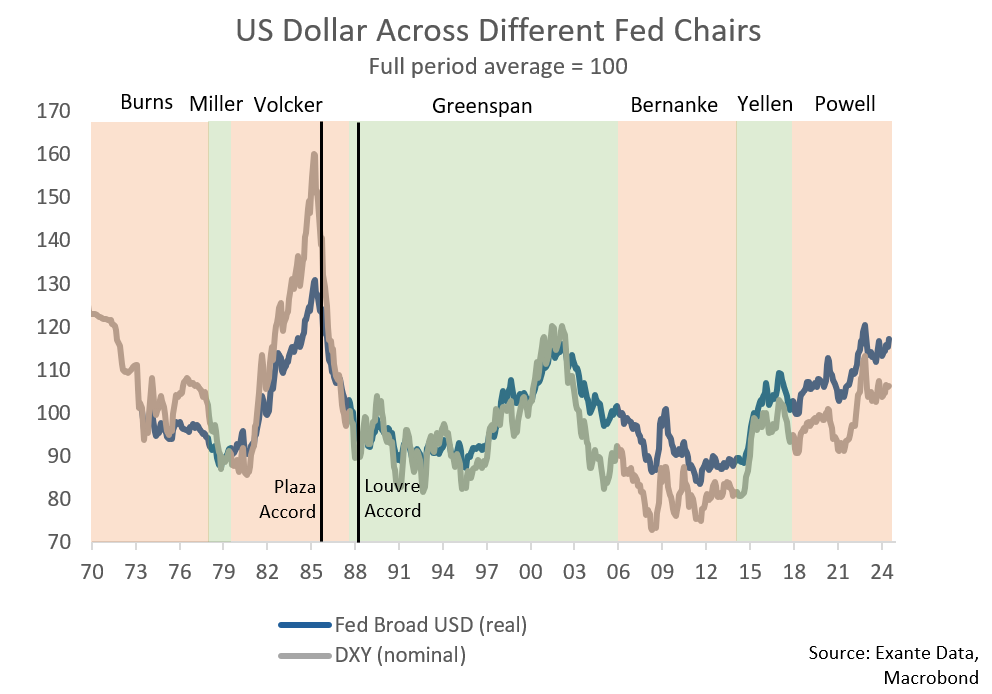

The chart below simply charts the evolution of the dollar during the last seven Fed Chairs. And it also marks the last two rounds of notable USD intervention: Around the Plaza Accord in 1985, and around the Louvre Accord in 1987.

For most of the 1970s, the dollar traded on a weakening trend (when Burns was Fed Chair), linked to rising trade deficits—with high oil prices a key factor—and low or negative real interest rates.

But the inflationary consequences were such that, by 1979, the appointment of Paul Volcker Fed Chair was followed by a notable monetary tightening as inflation control became the priority once more.

This was followed by the election of President Reagan in 1981 who sought to push US growth by lowering taxes, overseeing an expansion in the Federal budget deficit from roughly 3% of GDP in 1980 to about 6% in 1985.

The combination of tight money and loose fiscal brought substantial USD gains and a widening external current account deficit—the twin deficits—until around 1985 when excessive dollar strength came to dominate policy thinking.

Such was the concern that a meeting at the Plaza Hotel in New York City in Sept. 1985 between policymakers from the US, France, Germany, Japan and the UK resulted in an agreement to intervene to depreciate the US dollar against the currencies of the other participants.

The US dollar depreciation that followed over the next two years, a move that had already begun before the Plaza meeting itself, continued until Feb. 1987 when the Louvre Accord, as agreed in Paris by the same participants plus Canada, sought instead to halt the decline of the dollar and stabilise currencies.

Strong dollar

In the period that followed, the major economies learned to live with the reality of floating exchange rates.

By the 1990s the US embraced free-floating and minimal intervention in currency markets, in line with the general free market philosophy and the reality that rapid capital movements—and thus greater private sector financial fire-power—make currency interventions increasingly difficult.

By 1995, this free-floating embrace evolved under Treasury Secretary Robert Rubin as the “strong-dollar policy.” Rubin insisted that “a strong dollar is in our nation’s interest,” as part of the Clinton administrations focus market driven growth while furthering US interest globally via free trade and flexible capital flows.

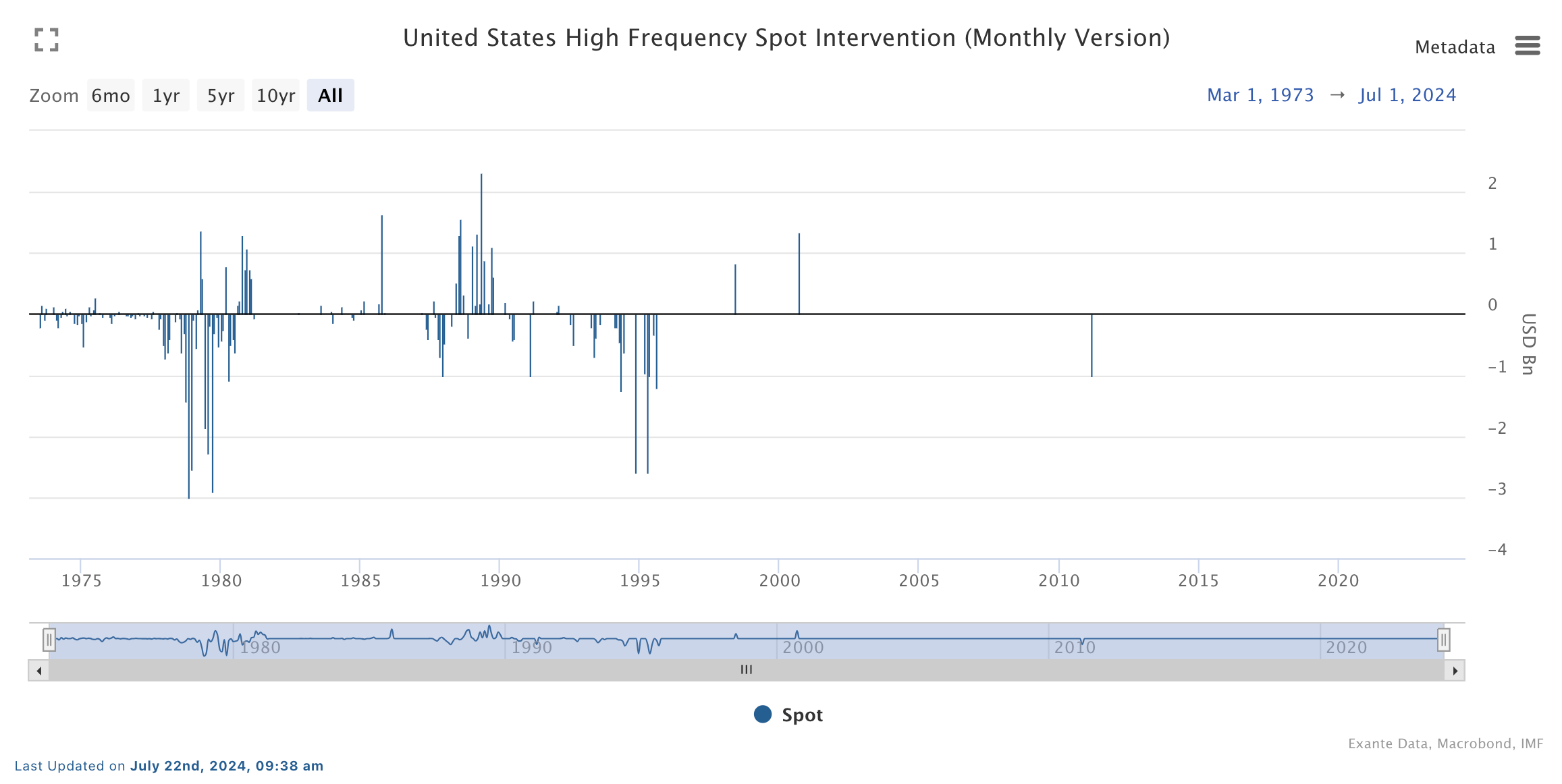

Since then, the US has generally adopted a non-interventionist stance to exchange rates.

We did have coordinated intervention in 2000 (to boost EUR) and in 2011 (to weaken JPY) but those interventions were tiny in size and largely symbolic (and not meant to move the USD on a broad basis).

Hence, it is fair to say that US Dollar policy has been non-interventionist since the mid-1990s, or for about 30 years; as illustrated in the chart below.

Further, in the period since the Great Financial Crisis there has been a G20 understanding in place in relation to currencies.

Cannes G20 Leaders' Declaration

By 2011, the Communique of G20 leaders expressed the commitment of all to ensure exchange rates were market-determined and to “refrain from competitive devaluations.”

We affirm our commitment to move more rapidly toward more market-determined exchange rate systems and enhance exchange rate flexibility to reflect underlying economic fundamentals, avoid persistent exchange rate misalignments and refrain from competitive devaluation of currencies.

And this statement reflects a longer-standing consensus within G7, that exchange rates should be market determined:

We, the G7 Ministers and Governors, reaffirm our longstanding commitment to market determined exchange rates and to consult closely in regard to actions in foreign exchange markets. We reaffirm that our fiscal and monetary policies have been and will remain oriented towards meeting our respective domestic objectives using domestic instruments, and that we will not target exchange rates. We are agreed that excessive volatility and disorderly movements in exchange rates can have adverse implications for economic and financial stability. We will continue to consult closely on exchange markets and cooperate as appropriate.

Statement by G-7 Finance Ministers and Central Bank Governors, February, 2013.

Of course, we might argue not all currencies have been equally flexible. But a constant since at least the 1990s has been the belief that a “strong dollar” is both good for the US and good for the world and that intervention is a bad thing. That is, until today.

Trump card

As the Presidential election gets closer, talk about the dollar is getting louder.

Yet Trump’s stance on the dollar is highly unusual, and a departure from the past US dollar policy noted above, although it is not a policy that is spelled out very explicitly.

Take Trump’s Bloomberg Businessweek interview last week. His very first comments as presented there were on the dollar:

Well, I think manufacturing is a big deal, and everybody that runs for office says you’ll never manufacture again.

We have currency problems, as you know. Currency. When I was president, I fought very strongly and hard with President Xi and with Shinzo Abe, who’s a fantastic man—actually, you know the story there.

So we have a big currency problem because the depth of the currency now in terms of strong dollar/weak yen, weak yuan, is massive.

But it is not only Trump. His new VP pick, JD Vance, has made similar noises about the need for a weaker dollar as a mechanism to boost manufacturing and exports. He told Politico, as reported in nymag, that a weaker dollar is good as it boosts US exports.

‘Devaluing’ of course is a scary word, but what it really means is American exports become cheaper, and that’s important. If you want to employ a lot of people in manufacturing, you need to make it easier for us to export and not just import what we need.

This populist twist turns US dollar policy on its head.

While for Summers 20 years ago the virtues of the “strong-dollar policy” were too obvious to spell out, for Trump-Vance a weak dollar is necessary to reverse the loss of manufacturing production to the rest of the world and reinvigorate the blue collar American.

But this twist leaves a number of things unspoken: first, how to achieve a weak dollar policy and against which specific currencies; and, second, what would be the cost of such a policy for the US domestically, and what are the implications for the rest of the world of such a change in regime. Part II and III of this series will touch on those issues.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.

It strikes me that regardless of what a Trump administration may want, markets may not oblige. currently, I would argue one of the key drivers of generic dollar strength is that there is so much USD debt outstanding outside the US, borrowers constantly need to get hold of dollars to service and repay that debt. those numbers, in the 10's of trillions of dollars, dwarf trade flows. the classic way to devalue a currency is to run loose monetary and tight fiscal policies in sync, but I dare anyone to explain to me the tight fiscal policies that a Trump administration will favor.

One has to wonder what the motivations are (other than ignorance) to implementing policy whose outcome directly undermines dollar-reserve status/ US hegemony. Rules based order al fuera? Trade-wars are easy to win? Idiocracy indeed.