Narrowing in on Eurozone broad money

Narrowing in on Eurozone broad money

A huge shift in Eurozone portfolios is on-going while credit creation has mostly paused. But does it matter?

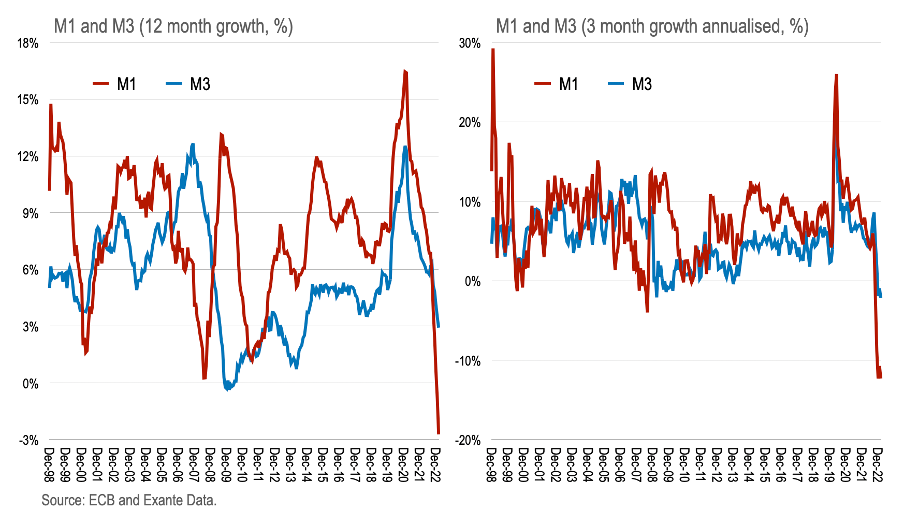

Narrow money (M1) in the Eurozone is collapsing as never seen before;

This reflects a shift from demand to time deposits as interest rates are normalising and banks lock in term funding (and is also an organic response to ECB balance sheet management);

But credit creation has also ground to a halt, recording the most negative credit impulse (change in credit provision) on record. This is more worrying. But even this might be more noise than signal in the post-pandemic world.

The revival of monetary aggregates as important signal following the pandemic continues.

We have discussed this in detail in a previous post “Lesson from The Great Reflation”, and we think policy makers will increasingly embed monetary dynamics in their analysis in coming months and years, even if they mostly ‘forgot’ to do so in 2020-2022.

After the significant run up in money during the pandemic, and subsequent pressure on asset prices and inflation, interest rates are now rising, prompting a shift in portfolios to higher yielding savings products.

Eurozone M1 collapse

Such portfolio behaviour was on display this week when the Eurozone monetary data showed M1 contracting 2.7% in the 12 months through Feb.; the past 3 months (annualised) is equivalent to a 12.3% decline (the same as the Dec. reading). This represents the largest annual contraction in M1 on record—and is sequentially far weaker than anything seen before.

Such contraction in M1 contrasts with the more modest behaviour of the broader measure of M3 which expanded 2.9% over the past 12 months and is sequentially contracting at 2.2%. This difference between M1 contraction against M3 expansion points to the transfer of demand deposits at Eurozone commercial banks to time and saving deposits.

Another way to see this is to show the 3-month flow in M3 broken into M1, M2 minus M1, and M3 minus M2. The rapid contraction in M1 over 3 months is about EUR1.5 trillion annualised though is offset by more than EUR1 trillion increase in M2 (minus M1) and M3 (less M2).

In other words, there is a shift in deposits occurring from demand to demand deposits to this with longer maturities (definitions for Eurozone monetary aggregates are available here.)

In any case, some contraction can be expected to facilitate QT which has now begun in the Eurozone—itself a form of portfolio adjustment.

Credit slowdown

On the asset side, which matters more for aggregate demand, banks continue to provide credit to households and non-financial corporates in aggregate (though in