The great energy recovery of 2022

The great energy recovery of 2022

The energy sector outperformed in the past year—and not only because of Russia-Ukraine

“By the fall of __, it was clear that a nation's prosperity, even its very survival, depended on securing a safe, abundant supply of cheap oil.”

When Albert Marrin penned this sentence in his book Black Gold: The Story of Oil in Our Lives, he was looking back nearly a century and referring to the fall of 1918. But we can agree now, looking at the wreckage suffered by the European economy and at severe disruptions elsewhere, that it applies just as well to the fall of 2022. The six months since the start of the Ukraine war have shown like no other recent period that the global economy in the 21st Century is still very much predicated, as it was in the 20th Century, on the story of oil (and natural gas), of nations searching for it, competing for it, trading it or withholding it.

This realization is not quite what we expected.

On the contrary, rich economies had been for over a decade moving slowly but methodically to reduce their dependence on fossil fuels. As a result of climate change concerns, investors were pouring money into renewables and curtailing fresh outlays to oil, gas and coal projects. Natural gas was previously seen as the cleaner source of energy but it was now deemed as only marginally better than oil. There was a spreading consensus in some quarters that fossil fuels were on their way out, sooner or later but preferably sooner.

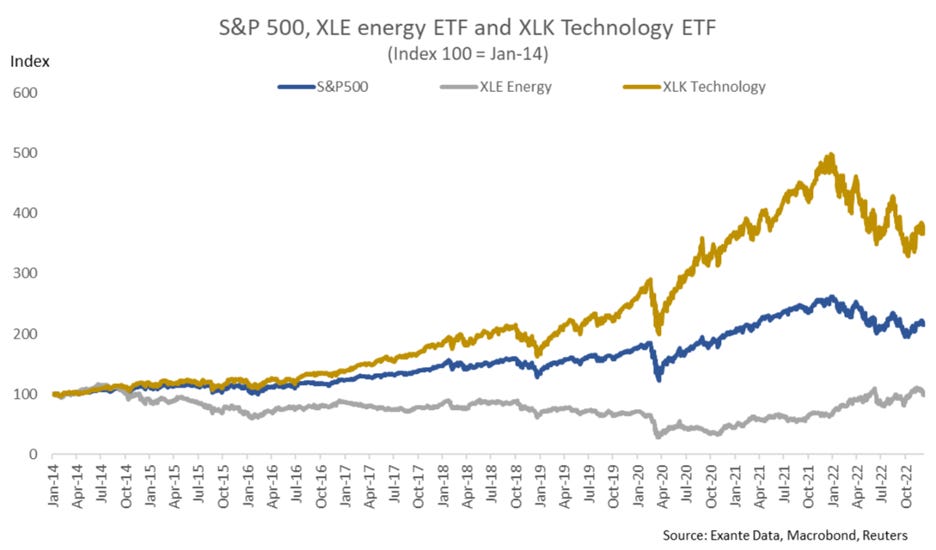

University endowments and other large institutions were scrubbing their portfolios free of fossil fuel holdings and were doing so with fanfare and as proof (in their view) of good responsible citizenship and of adherence to ESG standards. Their timing was good because, starting in late 2014, a surge in shale oil production in the United States depressed the price of oil and with it the price of energy stocks. From late 2014 to early 2020, the mere avoidance or diminution of fossil fuel holdings allowed many endowments and funds to deliver significant outperformance vs. the major equity indices. Their returns were further boosted by their generous allocations to the technology sector where stocks rose smartly year after year.

Consider that from its peak in June 2014 to the end of 2019, the XLE energy ETF declined by 40% while, during the same period, the XLK technology ETF rose by 142% and the S&P 500 by 92%. It is easy to see how many “clean” or “green” funds outperformed the S&P 500 in 2014-19, in particular if they overweighted the technology sector.

But linear assumptions are often shredded by reality. So then the pandemic came.

The stock market and all sectors crashed.

At the bottom of the panic, short-duration oil futures were briefly priced below zero as financial traders were desperate to get them off their books and to avoid taking physical delivery. Imagine in an extreme scenario a London fund manager being visited by an oil delivery truck at his Kensington townhouse. Luckily this did not come to pass.