The Suffering Sri Lankans

The Suffering Sri Lankans

Net official support under the IMF program will build international reserves rather than support vital imports; the "sudden stop" starts now.

IMF program and other official external financial support in coming years will be “spent” by the government but will not be “absorbed” through imports to support the ongoing humanitarian crisis;

Rather, central bank sterilisation and reserve accumulation will accompany these inflows and more—a buffer to help service generously restructured debt in outer years;

As such, the external financing “sudden stop” starts now; the economy will weaken further and current account swing to surplus.

The story of Sri Lanka’s demise combines pandemic-related travel disruptions, a global energy crisis, a dose of domestic corruption, and the overhang of external debt accumulated during calmer times—against bilateral creditors with geopolitical ambitions and private investors in search of yield.

The International Monetary Fund (IMF) program, agreed last month, has to unpick this legacy—dividing diminished prospects between legacy creditors and the next generation of Sri Lankans.

It also provides an important test for post-pandemic sovereign restructuring and burden-sharing at a time of immense hardship for many.

The program therefore deserves careful consideration to unpick the explicit or more often tacit assumptions that will determine Sri Lanka’s fate.

Unfortunately, the program does not hang together for a number of reasons.

But the main concern is as follows: the entire flow of net official external financial support under the program, from the IMF and other multilateral agencies, will build foreign exchange reserves rather than pay for vital imports. That is, while program funds will be notionally “spent” in support of fiscal policy they will not be “absorbed” through spending and the balance of payments. This has been explored in the context of development aid by staff inside the IMF and ought to be well understood—also discussed in a technical annex below. Instead, at a time of humanitarian crisis, Sri Lankan external support will be saved through central bank “sterilisation” operations, offering no meaningful support for the local economy.

This also implies the true “sudden stop” in external financing via the consolidated government starts now—as part of program design; the private sector must now rely on external funding from other sources. Yet the IMF’s track record when it comes to projecting private capital flows is poor to say the least.

Put another way, the program is stacked in favour of the few creditors at the expense of the suffering many. Meanwhile, as noted by Brad Setser at the Council on Foreign Relations, “the proposed debt targets appear to be so generous to creditors that they call into question the ability of a restructuring to return Sri Lanka to debt sustainability.”

We start with a brief summary of the main program assumptions before discussing the “spending” versus “absorbing” distinction—and finally some of the key domestic balance sheets judgments.

Program objectives

In terms of objectives, there are three. First, fiscal consolidation and debt sustainability, including through restructuring. Second, monetary and financial stability, including by restoring a healthy international reserves as buffer. Third, structural reforms, including to address corruption concerns. We are interested in exploring the first two objectives here.

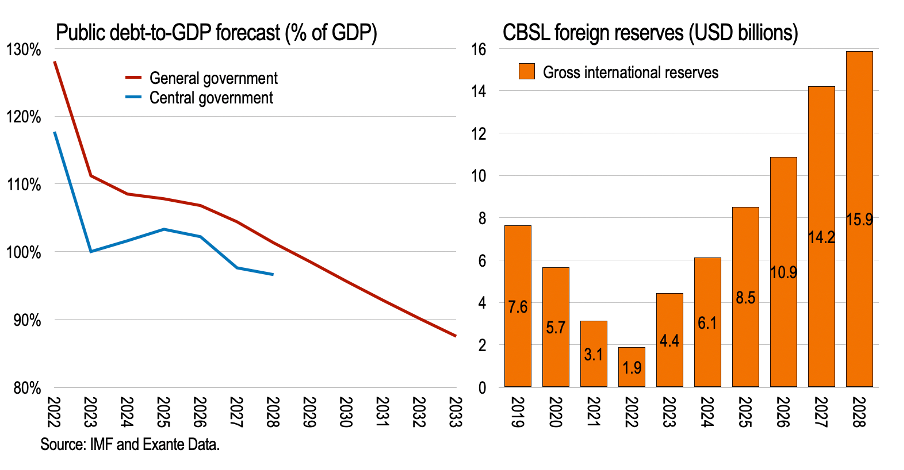

Seen in terms of program projections, the next chart summarises the main financial variables relating to the government—key targets over which the authorities have some, though certainly incomplete, control.

General government debt-to-GDP is expected to fall from 128% of GDP in 2022 to 107% in 2026 and 90% in 2032. The narrower definition of central government debt-to-GDP is expected to touch below 100% by 2027. This would leave central government debt to GDP, in the illustrative restructuring baseline, well above the 2019 level of 83% despite efforts to ameliorate this debt burden with international support.

Fiscal consolidation accompanies the debt reduction effort, of course, with the primary balance adjusting 6.1ppts, from -3.8% in 2022 to +2.3% in 2025. This is a large consolidation, mainly through revenues, and contrary to the fiscal stance of peers.

Turning to the Central Bank of Sri Lanka (CBSL), gross international reserves are expected to increase from about USD2bn as of end-2022 to about USD16bn in 2018—to more than double reserve holding in 2019.

This represents 15% of GDP reserve accumulation over 6 years.

Where do these reserves come from? The Staff Report explains they come “through outright FX purchases in the market, supported by a non-interest current account surplus, new external financing and other non-debt creating inflows, and sovereign debt relief.” (See ¶22 on p. 19.)

To “spend” or to “absorb”

Remarkably, pretty much all Fund program and associated official support will be channeled into the central bank’s international reserves—and not to finance imports.

They don’t tell you that in the Staff Report.

As elaborated in the technical annex, just because the international community is providing external financing as part of the program to be “spent” by the government, it does not mean such support will be “absorbed” as imports. Rather the absorption of external financing depends also on central bank actions. And in this case the Central Bank of Sri Lanka (CBSL) is assumed to accumulate a large buffer of international reserves—selling domestic assets in the process, de facto generating resident financing for the fiscal deficit.

This policy combination of fiscal adjustment and huge reserve accumulation, if carried out, will be extremely restrictive and choke off the entire flow of foreign exchange from official sources—the only source in recent years—to the private economy in the period ahead.

In this way, the sudden financing stop has just got very real indeed.

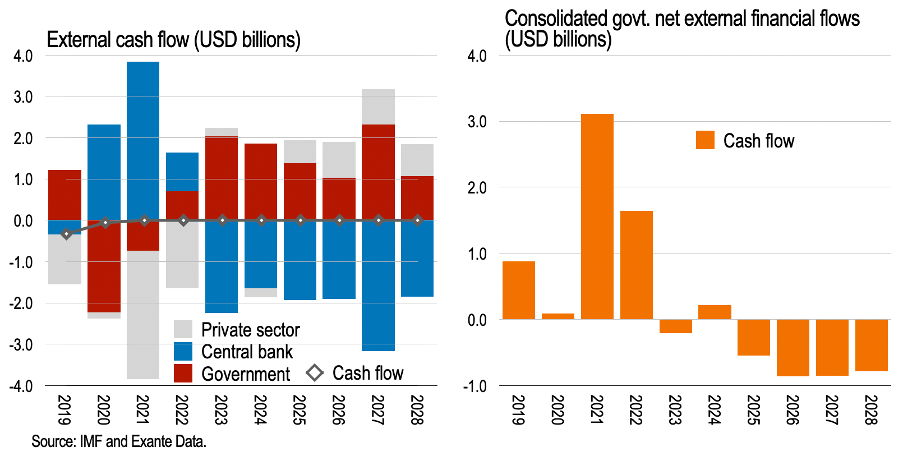

To see this, take the gross external financing table from the Staff Report (Table 4, p. 44) and extract the net external cash flows by sector—that is, ignoring the accrued debt relief.

What we see—per the chart below, a positive being a net inflow—is USD9.7bn in net external borrowing by the government over the next 6 years, some from the Fund but also other multilateral lenders as well as market access in later years, but USD12.7bn accumulation of net external claims, or outflows, by the central bank, largely due to the accumulation of foreign exchange reserves.

Consolidating these flows, right chart, CBSL will withdraw all external borrowing by the government and more over the program horizon—relying additionally on private financial inflows for sources of foreign exchange.

Indeed, the private sector is expected to swing from net external outflows in recent years to net financial inflows, after the current account deficit, of about USD3bn cumulatively—that is, more than needed to finance the current account deficit.

An alternative expression of this extraordinary sterilisation of external support is found by looking at the quantitative targets under the program—which are set for 2023 alone. Net international reserves (NIR) have a floor of minus USD1,592 million by end-2023 as a quantitative performance criterion under the program—an increase of USD1,948 million on end-2022 (see page 106). This number is derived from the macro-financial accounts adjusted for the authorities’ NIR definition—there are small discrepancies which we ignore here.

We can trace precisely the counterpart of this flow within the Gross External Financing table (page 46). Focusing on the government, we see IFI budget support in 2023 of USD900 million, net external borrowing of USD2,120 million (mainly bilateral and multilateral financing) while amortising USD986 million—or net external financing of USD2,034 million.

So the government will borrow (net) USD2,034 million in 2023, mainly from IFIs, multilateral and bilateral lenders, while the IMF tasks CBSL to accumulate net international reserves of USD1,948 million—leaving USD86 million residual to support the local population of 22 million over the next year; about 4 dollars per capita, or less than 8 cents per person, per week.

Contrast the World Bank’s latest summary of the situation:

The World Bank is deeply concerned for the people of Sri Lanka, as the country goes through the worst economic crisis in decades. We are repurposing resources from existing [ongoing] projects to support the most urgent needs, as well as working in coordination with other development partners in advising on appropriate policies to restore economic stability and broad-based growth.

Instead, it is as if multilateral lenders are setting up a trust fund at the CBSL for the holders of restructured debt under the guise of a humanitarian rescue effort.

A private offset?

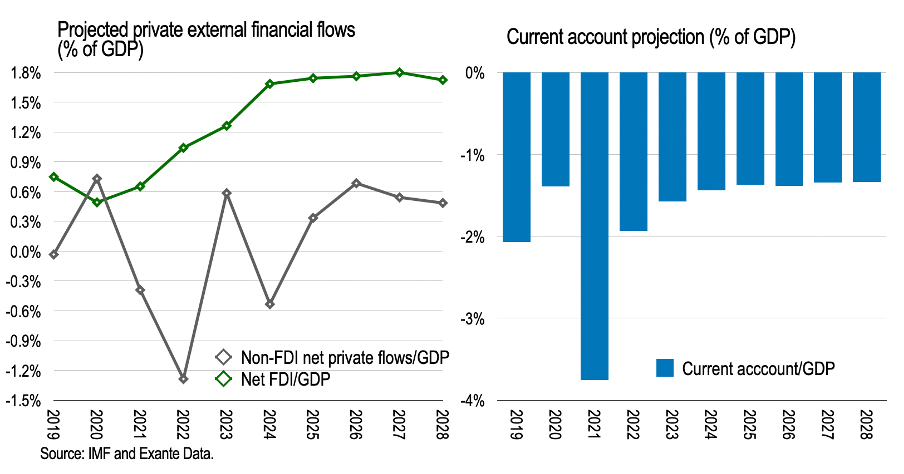

A recurring theme in IMF programs is the assumption that private external financing will spontaneously return to support activity despite austerity. Such was assumed initially in both Greece and Argentina, for example. For the private sector to do so is unusual into a downturn absent large asset price overshoot, and for this reason seldom materialises. In this case, the implied private saving-investment balance in Sri Lanka is expected to improve by about 1.5% of GDP per year on average over the next thee years—such that private spending on consumption and investment goods will provide an offset to austerity and the fx crunch.

Experience has shown that private spending does not accelerate into fiscal austerity—and the current account, initially at least, takes the full burden of adjustment by moving sharply into surplus, especially due to the external financing sudden stop.

Such adjustment is also associated with a deep recession and compression of domestic demand.

This seems like a more reasonable baseline.

The IMF projects real GDP growth this year of -3.0%, but after -8.7% in 2022 this requires a sharp sequential acceleration to offset large carry-over. In which case, the recovery is expected into the sudden stop!

But where might these apparently supportive, if unlikely, private financial inflows originate? Net FDI inflows are expected to roughly double from 2019 to nearly 1.8% of GDP in 2024 in perpetuity. Together with other private net inflows, this financing more than covers the assumed continuing external current account deficit—thus providing the additional foreign exchange for the accumulation by CBSL as reserves above the fx generated by the government, as well as paying for imports and what external interest payments remain.

Sustainability once more

We might finally note in passing some features of the sustainability assessment.

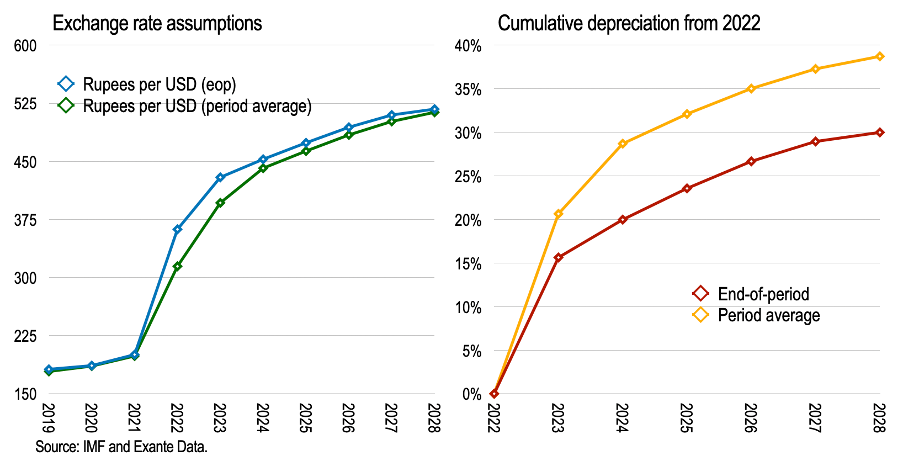

In Sri Lanka’s case, abut 50% of public debt is in FX at the beginning of the forecast—less than Argentina, but substantial still. And this will be added to, though there is no financing table for the general government in the program document. Nevertheless, exchange rate control will be important for this reason.

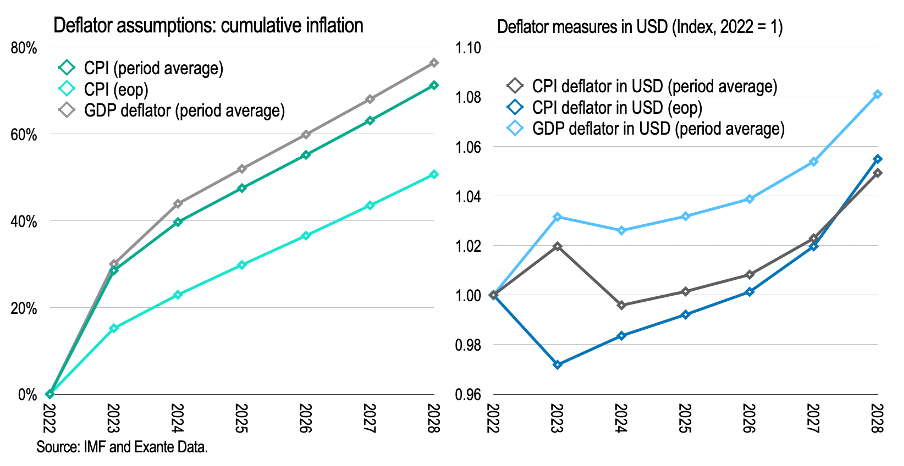

The implied path for the Rupee exchange rate under the program can be calculated from the ratio of Rupee to USD GDP for period average and banks’ net foreign assets in Rupees versus USD for end-period (eop).

From end-2022 to end-2028 the exchange rate is expected to depreciate by 30% or nearly 40% on a period average basis.

If we take the ratio of the price index to the appropriate eop or period average exchange rate index, we get a sense of the contribution of inflation (in decreasing) and the exchange rate (in increasing) the FX dominated debt—while the deflator alone erodes domestic currency debt.

As can be seen, the deflator outstrips future exchange rate weakness, allowing FX debtto-GDP to decline from this source.

Alternatively, the USD value of GDP is expected to increase by 19.4% from 2022 to reach USD89.9bn in 2028, slightly above the 2019 level.

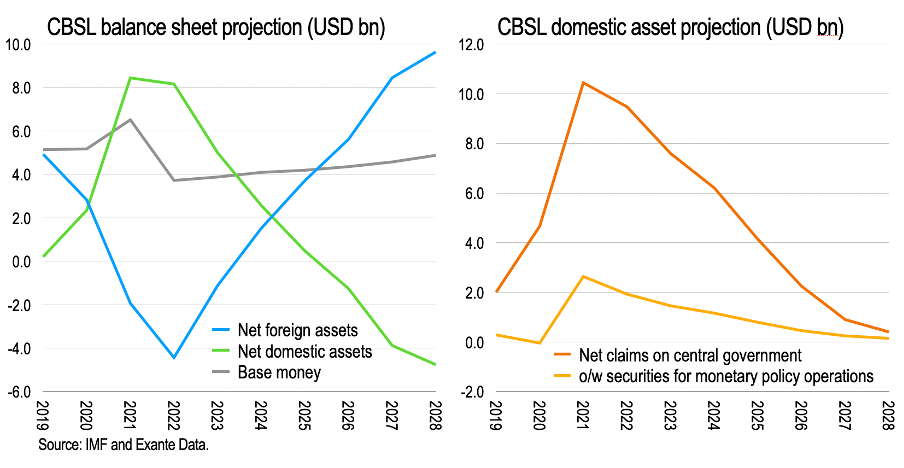

In the meantime the central bank balance sheet will be reshaped. How? Well:

the CBSL has started to downscale monetary financing and plans to offload holdings of treasury securities under the program, to support a normalization of its balance sheet and help prevent excessive money expansion, with close attention to reserve money growth. Under the program, monetary financing is envisaged only in the case of a shortfall in budget support from IFIs during the first 6 months of the program.

Looking at the balance sheet projection (converted into USD, page 43), the increase in net foreign assets is almost entirely offset by a decline in net domestic assets—so that the base money impact is minimal. And this decline in domestic assets is largely due to net claims on central government, which involves selling the outstanding stock of government and government guaranteed securities accumulated during the pandemic.

In this way, the increase in foreign exchange reserves involves an expansion in government debt held by residents—de facto domestic financing of the deficit.

The monetary survey as a whole, not shown here, sees only a modest decline in overall claims on government by the consolidated banking sector—that is, both commercial banks and the central bank combined. This implies CBSL will sell these securities to domestic banks, making them indirectly held by households and corporates through the growing broad money stock—only about half of which is due to expanding credit to corporations. The other half of the broad money increase is implicitly due to the deposit of financial inflows from abroad, net FDI inflows in particular, with banks.

Conclusions

As noted, the danger with this approach is that Sri Lanka is being starved of official sources of FX at a time of humanitarian crisis—and the associated foreign exchange reserve build up is being made available instead to support creditors who are subject to suspiciously generous restructuring terms.

Most likely the worst of the economic crisis is still to come as a result of this sudden stop as domestic demand will contract sharply, the current account swing into surplus—before stabilisation and growth can begin.

At that stage, foreign exchange will be plentiful—again helpful for external creditors. But the damage to the economy in the meantime could undermine the debt sustainability assumptions on which the program is based to begin with. And the opportunity will be lost for a fairer sharing of the burden of adjustment.

Annex: spending does not mean absorbing external financial support

It’s strange to internalise and so often gets overlooked, but external financial support can be sometimes be “spent” by the fiscal authorities but never “absorbed” as imports through the balance of payments—instead accumulated as international reserve assets.

This is something explored in the context of aid transfers in this useful IMF paper, the key point being from the abstract:

On the policy front, it [is important to] distinguish… between spending the aid, which is controlled by the fiscal authority, and absorbing the aid—financing a higher current account deficit—which is influenced by the central bank's reserve accumulation policies.

We show this here by using a very simple set of accounting relations; though stylised, it will make our point about the Sri Lanka program.

Start with the balance of payments. The current account (or, using a slight abuse of definition, nominal exports minus imports, CA = X - M) equals the change in government (net) foreign liabilities (dFL) plus change in reserve assets (dR) of the central bank:

CA = X - M = -dFL + dR

This ignores private external financing, of course, to keep things clear.

The fiscal deficit is financed by foreign liabilities, as above, debt issued to residents (dDL) and to the central bank (dCB):

FD = dFL + dDL + dCB

While the change in the base money liabilities of the central bank (dH) equals the change in domestic assets (or central bank claims on the government, as above) and in foreign assets (international reserves, as above):

dH = dCB + dR

To best illuminate the distinction between spending and absorbing, to these three constraints we add three assumptions—assumptions which reasonably approximate the Sri Lankan case. First, assume base money is unchanged (dH = 0). Second, assume the fiscal deficit is equal to net external financing of the government (FD = dFL). And, third, assume the central bank follows a rule whereby they sterilise some fraction n of net external financing of the government (dR = n*dFL).

Imposing these assumptions, while taking exports and the fiscal deficit to be exogenous, it is straightforward to derive two interesting expressions.

First, from the balance of payments and monetary accounts, nominal imports are equal to exports plus some fraction of external financing of the government:

M = X + (1 - n)*dFL

Second, from the fiscal and monetary accounts, the accumulation of claims on the government by residents is some fraction of the government’s net external financing despite the fact the fiscal deficit is entirely financed from abroad:

dDL = n*dFL

Notice how the central bank is the key link to both the BOP and domestic financing.

And in the presence of external financial support to the government, the domestic private sector can either end up absorbing this external financing as imports (in excess of nominal exports) or saving this through claims on the domestic government. The central bank’s sterilisation parameter, n, determines the convex combination of the two.

Indeed, summing the two expressions we get M + dDL = X + dFL = X + FD.

The fiscal deficit (FD) and nominal exports (X), both exogenous, determine the overall resource envelope for the private sector; monetary policy—through sterilisation—determines the split between imports (absorption) and saving through claims on the government.

In fact, looking “beneath the hood,” the government is borrowing from abroad to finance the fiscal deficit, converting to domestic currency for spending in local money markets. But the central bank is sterilising some or all of this by releasing claims on the domestic government, changing the structure of their balance sheet by shifting between domestic and foreign assets, equivalent to a tightening of monetary policy.

In the extreme case where n = 1, close to the case of Sri Lanka as outlined above, none of the government’s net external borrowing is released to finance imports— which are thus constrained to equal in value exports as the central bank emits financial claims on the government and withdraws demand and absorption from the economy.

The government and international community might believe they is financed exclusively by non-residents, supporting their humanitarian credentials. But what foreign creditors give, the central bank can take away. And the central bank, through sterilisation, ensures the consolidated government is instead financed entirely by residents, diverting such external resources instead to foreign reserves assets.

This combined fiscal-monetary stance is far “tighter” than implied by looking at the fiscal deficit alone—which is itself quite the straightjacket; the private sector is in fact experiencing a sudden financing stop.

In other words, careful analysis should distinguish between spending and absorbing external financial support—only the latter ensures resources from foreign aid, or from an IMF program, are available to support those most in need of humanitarian or developmental support. Only through the combined central bank and fiscal balance sheet does the true policy stance unfold.

The content in this piece is partly based on proprietary analysis that Exante Data does for institutional clients as part of its full macro strategy and flow analytics services. The content offered here differs significantly from Exante Data’s full service and is less technical as it aims to provide a more medium-term policy relevant perspective. The opinions and analytics expressed in this piece are those of the author alone and may not be those of Exante Data Inc. or Exante Advisors LLC. The content of this piece and the opinions expressed herein are independent of any work Exante Data Inc. or Exante Advisors LLC does and communicates to its clients.

Exante Advisors, LLC & Exante Data, Inc. Disclaimer

Exante Data delivers proprietary data and innovative analytics to investors globally. The vision of exante data is to improve markets strategy via new technologies. We provide reasoned answers to the most difficult markets questions, before the consensus.

This communication is provided for your informational purposes only. In making any investment decision, you must rely on your own examination of the securities and the terms of the offering. The contents of this communication does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. Exante Advisors, LLC, Exante Data, Inc. and their affiliates (together, "Exante") do not warrant that information provided herein is correct, accurate, timely, error-free, or otherwise reliable. EXANTE HEREBY DISCLAIMS ANY WARRANTIES, EXPRESS OR IMPLIED.

Very interesting piece! I'd argue the deep contraction is well underway since late 2022, and that it's getting reflected in increasing current account surpluses already. Gov also seems to have an expectation of a lower CA balance than the IMF does (CBSL AR) though at a stronger currency level.

Though of course, if SL truly wants to issue an ISB, the current levels won't be enough. For the exact same points you make, think very difficult for SL to actually do so once the time comes - the coupon will be far too high to justify it. If SL DOES perform well enough to justify a power coupon through higher exports for example, then that might not be an issue as a result.

The other side of the coin would be the credit situation in the private sector, which might be crowded out anyway with the 6% of GDP recapitalization needs estimated by the IMF (even if it is just a quarter of that, that would still lead to the current credit contraction continuing and then only recovering slowly). Wonder if that leads to greater development of repos and trade lending, which then encourages the export side. Possibly wishful thinking.

Very insightful in terms of the explanation on connecting the NIR targets and expected financing flows in the IMF staff report for Sri Lanka. The adjustment and contraction is definitely already underway. In 4Q 2022, GDP contracted 12.5% and current account was a small surplus in both 3Q & 4Q. And we think a surplus is likely in 1Q 2023 as well.

Since Aug 2022 the central bank has been on monthly net purchases of FX from domestic market, absorbing just over $1 billion, with March 2023 seeing about $400mn - most of which happened even before the IMF first tranche came through. In fact about a third of the first tranche was used to repay part of an Indian credit line obtained in 2022. And we think about $800-900mn in central bank liabilities need to be repaid in rest of 2023 also - esp a swap from Bangladesh and part of the ACU trade liabilities.

I touch on some these in https://macrocolombo.substack.com/p/how-did-sri-lanka-manage-to-boost and https://macrocolombo.substack.com/p/india-as-lender-of-last-resort-to