What are Argie bonds worth now?

What are Argie bonds worth now?

As the end-game approaches, another large haircut for bondholders looms

When the history of Argentina’s recent crisis is written, it will have to answer the vexing question why it took so long to restore stability and sustainability—how monetary control was lost and inflation accelerated to triple digits despite the oversight of the international community and a record dollop of cash.

But this will be for some brave historian to ponder.

For now, the immediate future will be shaped by two recent developments that suggest the end-game is near—developments that provide at last an opportunity to restore monetary control.

The first, of course, is the growing support for the libertarian economist Javier Milei as candidate for President in the forthcoming elections. Anyone who invokes the transversality condition on the campaign trail must be bold enough to meet the sustainability challenge!

The second, perhaps more important, development is the recapitulation in the IMF’s latest program document of need to recapitalize the central bank (BCRA) in the form of a structural benchmark by end-Oct (see page 93). In particular, the authorities have agreed to:

Develop in consultation with Fund staff, a strategy to durably improve the BCRA financial position, drawing on recommendations from the Fund’s Safeguard Assessment

While this benchmark has, since 2018, slipped more times than Bambi, it is reasonable to hope that this time will indeed be different.

For one thing, the politics of inflation and the manifest monetary-fiscal failings have become mainstream—hence Milei. For another, the timing of this benchmark is presumably no coincidence—with a deadline after the election but before the new government is formed.

Done properly, this recapitalisation will realise the quasi-fiscal deficit and bequeath the new administration a substantially worse fiscal position to which they will then be forced to respond. Only at this point, with the scale of the fiscal challenge laid out in full for the incoming administration, will the Fund need to decide whether political commitment is there to meet the challenge—or to pull the plug on the whole adventure.

As an aside, assuming the program indeed continues it is reasonable to rule out dollarisation simply because it is unlikely to receive any support from either side of 19th Street. On the other hand, if the program lapses then unilateral dollarisation becomes more realistic a possibility—alongside default on official commitments, private debt, and the banking system.

Consolidated fiscal fright

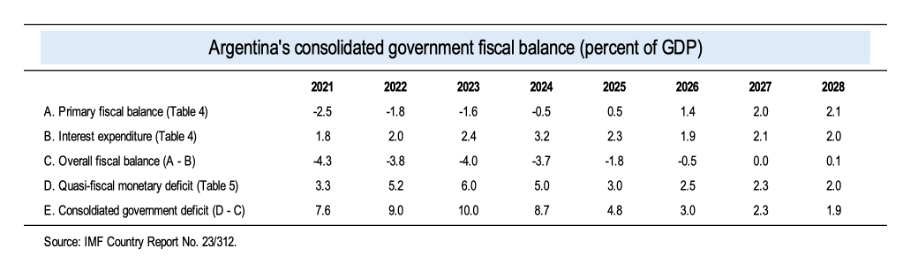

Back to the true fiscal position. We can further consult the latest IMF document and combine the projected fiscal deficit with the monetary deficit from the central bank survey (the quasi-fiscal deficit) as in the table below. We get the consolidated government deficit at 10 percent of GDP this year declining to 8.7 percent of GDP next year and 4.8 percent of GDP in 2025.

In this forecast, more than half the adjustment of the consolidated government deficit over the next two years comes about due to the spontaneous reduction in the central bank’s deficit.

Based on nothing but wishful thinking, there is reason to believe these forecasts are optimistic and the true fiscal position throughout the decade will be much worse, as we now project. But in any case, the end-Oct. recapitalisation should make these projections stale as the quasi-fiscal deficit is handed back to the central government—at which point another debt operation will be needed to restore fiscal sustainability and all the other assumptions up-ended.

Back of the envelope sustainability calculations

If we consolidate the government and central bank, what does this tell us about the likely actions needed to restore sustainability?

Argentina’s public debt redemption profile includes about USD70bn that ought to be repaid to BCRA, as in the redemption profiles below. And most of this debt is in foreign currency, meaning sustainability requires monetary control.