Italian households keep the faith

Italian households keep the faith

BTPs have been supported by deposit rotation

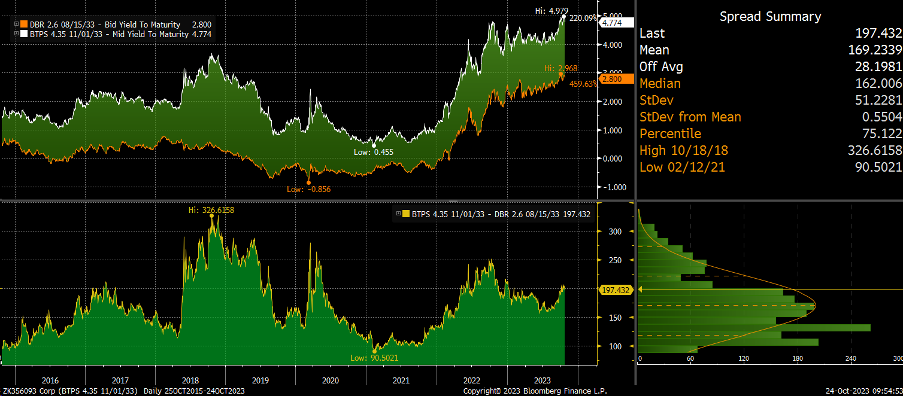

Italian yield spreads have been “well behaved” over the past year despite the surge in global yields—with the spread to bunds contained below 200bps;

Net ECB purchases from the PEPP picked up in the Spring of 2022, but have since been a fairly small and cannot explain BTP performance;

The big buyers have been Italian households and corporates, who have rotated out of broad money into direct holdings of government securities.

A noteworthy development over past six months has been the performance of Italian government bond yields, or BTPs. To be sure, as elsewhere, yields have increased since the pandemic to reach highs not seen since 2012. But the BTP yield spread to bunds has been contained for most of the past year, good news for the Eurozone.

For example, the BTP-bund spread has remained below 200bps throughout the year, even dipping close to 150bps before in the summer. This compares with a spread of closer to 300bps following the political disruptions of 2018. A 300bps spread at this time would put 10Y yield near 600bps, further damaging prospects for public debt sustainability which hangs in the balance.

It’s not the ECB

The obvious place to look for the performance of BTPs is the European Central Bank (ECB) which has kept open the option of flexible purchases, deviating from capital key, under the Pandemic Emergency Purchase Program (PEPP.)